Self-employed individuals declare salaries tax or profits tax based on whether they have an employment contract; if both apply, they must declare both simultaneously. Business-related expenses and mandatory MPF contributions (capped at HK$18,000) are tax-deductible. Even if income is below the tax exemption threshold or there are business losses, declarations must still be made on time.

Summary of key points

- Self-employed individuals declare salaries tax (employed) or profits tax (self-employed) depending on whether they have an employment contract; if both apply, they must declare both simultaneously.

- Even if income is below the tax exemption threshold or there are business losses, declarations must still be made on time, otherwise it may be considered tax evasion.

- Business-related expenses (rent, equipment, advertising, etc.) and mandatory MPF contributions can be deducted for profits tax.

- After receiving the tax return, it must be submitted within one month; if the tax return is not received, the tax authority must be notified proactively within four months after the end of the tax year.

Who qualifies as a self-employed individual?

Individuals who sell goods or provide services in their own name and profit from it, without a fixed employer, are considered self-employed individuals (Freelancers). Common types include:

- Owners of online stores or IG shops

Selling goods in one's own name, whether online or physical, as long as they are not employed by others, falls under this category.

- Business Partners

Co-managing a business with others (such as tutoring centers, photography teams, nail studios), earning income from partnership business.

- Freelancers

Without a fixed employer, taking on projects independently, commonly seen in industries such as designers, writers, photographers, illustrators, translators, fitness coaches, etc.

- Temporary part-time (casual work)

Accepting short-term jobs such as exhibition staff, event assistants, substitute teaching, etc., without a long-term employment relationship.

What taxes do self-employed individuals need to report?

The tax reporting for self-employed individuals in Hong Kong is divided by employment contracts: those with a fixed employer report salaries tax, while those taking on projects or running a business report profits tax; if both apply, they must declare both simultaneously. Even if income is below the tax exemption threshold, the tax return must still be submitted on time.

Tax reporting is based onWhether an employment contract existsAs the criterion for judgment:

| identities | Reported taxes |

|---|---|

| Employed by a company (with an employment contract, fixed salary, and mandatory MPF contributions) | salaries tax |

| Self-employed or freelance (without an employment contract) | profits tax |

| Simultaneously has employment income and self-employment income | Salaries tax + profits tax |

Three examples of self-employed individuals filing taxes

Alen: Full-time marketing personnel, takes freelance jobs after work, clients pay directly via bank transfer. → Must declareSalaries tax + profits tax

Ken: Freelance photographer, no employment relationship, develops clients and sets fees independently. → Must declareprofits tax

Zoe: Part-time tutor at a language center, works two days a week, no other income. → Must declaresalaries tax

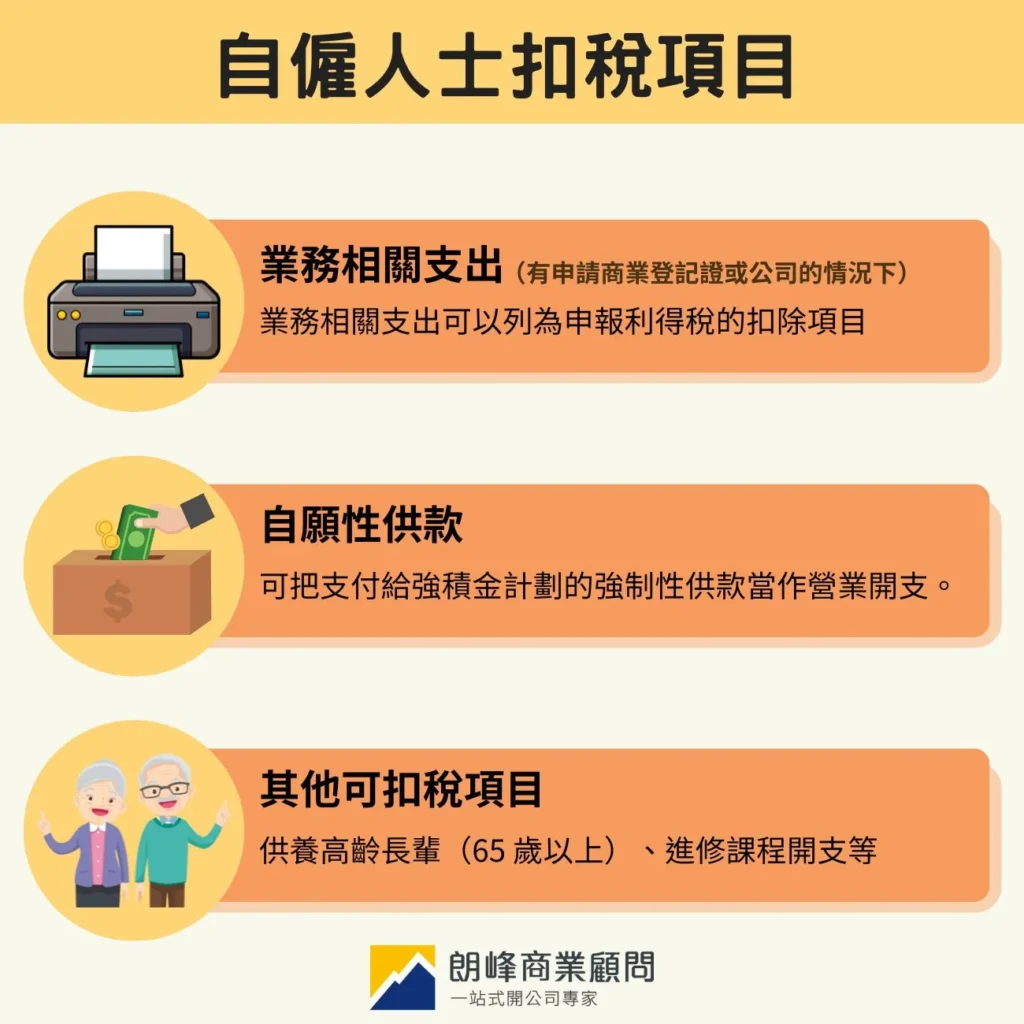

Tax deduction items for self-employed individuals

Business-related expenses

When declaring profits tax, any expenses that can be proven to be directly related to earning business income can be claimed as deductions. Common items include:

- Operating Costs for Provision of Services

- Advertising and marketing expenses

- Equipment and Facilities for Business Use

- Incoming goods and related purchase costs

- Accounting and Tax Consultancy Fees

- Office rent, utilities, and communication expenses

It is crucial to keep all receipts and payment records. When the tax authority conducts checks, proof must be provided to demonstrate that the expense is indeed related to the business.

Mandatory MPF contributions

Mandatory contributions made by self-employed individuals to the MPF scheme can be deducted as business expenses when filing profits tax, with a cap of HK$18,000 per tax year.Voluntary contributionsGenerally non-deductible (except for voluntary contributions that are deductible).

Personal tax allowance and other deductible items

Self-employed individuals are also entitled to the basic personal tax allowance and other deductible items (such as personal education expenses, voluntary health insurance premiums, etc.), see details.Complete guide to calculating salaries tax and personal tax exemptions.。

The tax exemption arrangement for married individuals can be referred to.Tax exemptions for married individuals and strategies for joint filing.。

Comparison of tax returns for different statuses.

| identities | Tax Returns |

|---|---|

| Sole proprietorship. | BIR60 (Individual Tax Return) |

| Incorporated | BIR51 |

| Non-corporate business | BIR52 |

| Businesses carried on by non-Hong Kong residents | BIR54. |

| Contract workers | IR56M. |

How to report without a business registration?

Any form of profit-making business in Hong Kong must obtain a business registration certificate. If not yet processed, a tax return must still be filled out and submitted to the tax authority. Income earned without any employment relationship and without holding a business registration must be reported under salary tax.

For information on the business registration application process, please refer to.Business registration certificate application guide.。

How to report with a business registration?

Those who have completed business registration will receive a profits tax return, which must include total income, total expenses, and deductible items for the entire year, along with invoices, receipts, and transfer records as supporting documents for the report.

Operating in the name of a company requires hiring an accountant for auditing.

Those operating in the name of a limited company, regardless of income level, must submit audited financial statements annually according to the Companies Ordinance, with an audit report issued by a licensed accountant and submitted with the profits tax return. The company tax filing process is more complex than that of individuals, involving documents such as balance sheets, profit and loss statements, and expense details, but allows for greater tax planning flexibility. For details, please refer to.Longfeng Accounting and Auditing Services.。

Six-step process for self-employed individuals to file taxes.

The tax filing process for self-employed individuals in Hong Kong consists of six steps: receiving the tax return, organizing income and expenditure records, calculating deductible items and taxable profits, filling out and submitting the tax return, paying taxes (generally in two installments), and continuing to keep accounts for the next year. The entire process can be handled online (eTAX) or in paper form.

Step 1: Receive the tax return.

The tax authority generally sends out tax returns or notifications via eTAX at the beginning of May each year. Self-employed individuals usually receive the personal tax return (BIR60); those operating as a company receive the profits tax return (BIR51).

Step 2: Organize business income and expenditure records.

Organize all customer payments (cash, bank transfers, Faster Payment System, etc.) and business-related expenses from the previous tax year, and prepare receipts, invoices, and transfer records.

Step 3: Calculate taxable profit

Total income minus operating expenses results in net profit; then deduct eligible tax items to arrive at taxable profit, which is the basis for determining whether to pay taxes and the amount of tax.

Step 4: Fill out and submit the tax return

You can choose to mail a paper form or file online.Tax easyFor those using paper forms, be mindful of the mailing time, as the tax authority calculates timeliness based on the receipt date rather than the mailing date.

Step 5: Waiting for tax bill and paying tax

The tax authority generally issues a formal tax bill within two months of receiving the tax return, and taxes are usually paid in two installments:

| Installment | General tax payment deadline |

|---|---|

| first tranche | Before mid-January |

| second phase | Before early April |

Step 6: Continue bookkeeping to prepare for the next year

It is recommended to keep regular records and save receipts throughout the year, rather than scrambling to organize them only during tax season. Complete income and expenditure records not only make tax filing more time-efficient but also help grasp the business operation status.

Consequences of late filing

According to Hong KongSection 51 of the Inland Revenue Ordinanceself-employed individuals have the responsibility to proactively notify the tax authority of their taxable income; not receiving a tax return does not exempt the obligation to file; failure to report accurately may result in tax recovery and penalties, and intentional tax evasion may lead to criminal prosecution.

Many self-employed individuals mistakenly believe that not receiving a tax return means they do not need to file; in fact, Section 51 of the Inland Revenue Ordinance clearly states that taxpayers have the responsibility to proactively notify the tax authority of their taxable income.

Handling of not receiving a tax return: You must proactively notify the tax authority in writing within four months after the end of the assessment period for the tax year.

Consequences of not filingAfter being discovered, all unreported annual taxes and corresponding penalties and interest must be paid; if deemed to be intentional tax evasion, the tax authority may initiate criminal prosecution, affecting credit records and future tax reporting.

Frequently Asked Questions

If income is below the tax exemption threshold, is it still necessary to report?

Yes, it is necessary. The exemption threshold determines whethertaxes are to be paid, while the obligation to report exists independently. As long as business activities are conducted, one must report to the tax authority; otherwise, it may be considered tax evasion.

If a company incurs business losses, is it still necessary to file taxes?

Yes, it is necessary. Limited companies must submit audited financial statements and profit tax returns every year, regardless of profit or loss; this is a legal obligation and is not exempted due to losses.

If a part-time company has already reported my salary tax, do I still need to report the self-employed portion separately?

Yes, it is necessary. The tax authority will not automatically combine the two parts of income; self-employed income must be reported separately for profit tax. If there is no self-employed income at all, it must still be filled out and confirmed in the tax return to complete the reporting process.

If I find that I have filled out incorrect information after submitting the tax return, can I correct it?

Yes, you can. You can send a written change notification or log into the eTax platform to use the "Correct Tax Reporting Information" function to submit a request. It is advisable to handle it as soon as possible to avoid complications if the tax authority has already calculated the tax bill based on the incorrect information.

Conclusion

The core principles for self-employed individuals filing taxes:Regardless of income level or business profit and loss, one must report on time.Based on this, properly organize business income and expenditure records and make good use of legal deductions to reduce tax burden while remaining compliant.

If you need assistance in organizing accounts or handling tax filing, you can learn moreLongfeng Tax Filing Services, or directly contact the Longfeng Business Consulting Team for inquiries.

Extended Reading

Complete guide to calculating salaries tax and personal tax exemptions.

Tax exemptions for married individuals and strategies for joint filing.

Hong Kong Profit Tax Filing Guide

Calculation of provisional salary tax

Last updated: May 2026.