Provisional tax is the estimated tax for the next year based on the previous year's income assessed by the tax authority, and the government's one-off relief does not apply to provisional tax. If the next year's income is expected to decrease by more than 10%, or if there are new tax exemptions not reflected in the tax bill, an IR1121 application for deferral can be submitted 28 days before the tax payment deadline.

Summary of key points

- Provisional tax is the estimated tax for the next year collected in advance from taxpayers by the tax authority based on the income of the previous assessment year, applicable to salaries tax, profits tax, and property tax.

- Calculation method: Based on the tax payable from the previous year, estimated without deducting the government's one-off relief in advance.

- The one-off relief for the 2025/26 assessment year (capped at HK$3,000) only applies tothe final assessment., and does not apply to provisional tax. If the next year's income decreases by more than 10%, or meets other statutory conditions, an application can be made to defer all or part of the provisional tax.

- Application deadline: 28 days before the tax payment deadline, or within 14 days after the tax bill is issued, whichever is later.

What is provisional tax?

Provisional tax is based on Hong KongInland Revenue Ordinance, where the tax authority estimates and collects the tax for the next year based on the taxpayer's income from the previous assessment year.

Hong Kong's provisional tax operates on a "pay first, calculate later" basis, where the provisional tax paid will offset the tax payable after the formal assessment of the next year; any surplus will be carried forward to offset the next assessment. Provisional tax must be paid for salaries tax, profits tax, and property tax.

After the formal assessment for the next year is completed, the provisional tax paid will first offset the tax payable for that year; if there is a balance, it will be carried forward to the next assessment; if it is insufficient, the difference must be paid.

Provisional tax for salaries tax is usually issued together with the final assessment tax bill, paid in two installments: the first installment is generally due before mid-January, and the second installment before early April. The specific payment dates are indicated in red on the tax bill.

Why is the provisional tax amount sometimes higher than the actual tax payable?

Many taxpayers find that the provisional tax amount is higher than expected after receiving the tax bill, the reason being:

The tax authority generally does not deduct the government's one-off tax relief in advance when calculating provisional tax, which can only be applied after the budget proposal is passed and legislated.

For the 2025/26 year, although the budget proposal suggests a relief of 100% for salaries tax (capped at HK$3,000), this relief only applies to the final assessment for the 2025/26 assessment year and does not apply to the provisional tax for that year; taxpayers must still pay the provisional tax on time and will receive a deduction during the assessment.

💡 Longfeng reminds you: If you see that the provisional tax amount is high when you receive the tax bill, there is no need to worry. After the next year's assessment is completed, any overpaid amount will be automatically carried forward or refunded, which is a normal mechanism.

Calculation method for provisional tax.

4. salary tax provisional tax.

After deducting various deductions from the salary income of the previous assessment year, estimate the tax payable for the next year at the same tax rate.

Last year's salary income - various deductions = Estimated basis for provisional tax.Provisional salary tax is estimated based on the salary income of the previous assessment year minus various deductions; provisional profits tax is calculated based on the assessable profits of the previous year minus allowable losses. Neither reflects the government's one-off tax relief for the current year in advance.

Provisional profits tax.

Estimated based on the assessable profits of the previous year, minus allowable losses.

Provisional property tax.

Estimated based on the assessable value of the property from the previous year.

Consequences of late payment of provisional tax.

| Situation. | Consequences. |

|---|---|

| Overdue payment. | Additional charge of 5% on the total taxable amount. |

| Overdue for more than 6 months without payment (including 5% additional charge). | An additional charge of 10% will be imposed. |

| Continuous non-payment. | The tax authority may issue a tax recovery notice to employers, banks, or debtors. |

| Serious circumstances. | The tax authority may file a civil lawsuit in the regional court to recover the outstanding amount and court costs. |

| Intention to leave Hong Kong. | The tax authority may apply to the regional court to prohibit the taxpayer from leaving the country. |

| Deliberate tax evasion | Criminal offense, upon conviction, can be sentenced to a maximum of three years in prison, and must also pay a fine |

Under what circumstances can one apply for deferred provisional tax payment?

If unable to pay on time due to financial difficulties or other statutory reasons, one can apply to the tax authority for deferred payment of part or all of the provisional tax. The statutory reasons for each tax type are as follows:

Conditions for deferring salary tax (meet one of the following)

- The assessable income for the next year is less than or may be less than 90% of the previous year

- Entitled to a tax exemption not calculated in the provisional tax notice (such as newborn child tax exemption, additionalDependent Parent Allowanceetc.)

- Will incur personal education expenses, approved retirement plan contributions, housing rent, residence loan interest, voluntary medical insurance premiums, qualifying annuity premiums, or deductible MPF contributions in the next year, and the amount exceeds the specified amount of the previous year

- Has ceased or will cease to earn assessable salary tax income before the end of the provisional tax assessment year

- Has lodged an objection to the salary tax assessment for the previous year

Conditions for deferring profits tax (meet one of the following)

- The assessable profits for the next year are less than or may be less than 90% of the previous year (must attach accounts draft signed for not less than 8 months)

- The amount of losses carried forward to offset in that assessment year has been omitted or is uncertain

- Has ceased or will cease business operations before the end of the assessment year

- Has opted for personal income taxation for the provisional tax assessment year, and may pay less tax under this method

- Has lodged an objection to the profits tax assessment for the previous year

Conditions for deferring property tax (meet one of the following)

- The assessable value of the property for the next year is less than or may be less than 90% of the previous year

- Is no longer or will no longer be the owner of the property before the end of the assessment year

- Has opted for personal income taxation for the provisional tax assessment year, and may pay less tax under this method

- 1. Opposition has been raised against the property tax assessment for the previous year.

2. The most common reason for applying for a deferral of provisional salary tax is that the expected income for the next year is reduced to below 90% compared to the previous year, or there are tax allowances (such as the new dependent parent allowance) not calculated in the provisional tax notice. Meeting the criteria does not guarantee full exemption; the tax authority will assess the amount that can be deferred based on actual circumstances.

3. Methods for applying for deferral of provisional tax.

4. Application deadline.

5. The following two dates,6. with the later date prevailing.:

- 7. 28 days before the deadline for paying provisional tax.

- 8. Within 14 days after the tax bill is issued.

9. If the provisional tax is paid in two installments, an application for deferral can still be made for the second installment even if the first installment has been paid, but the above deadlines must be adhered to.

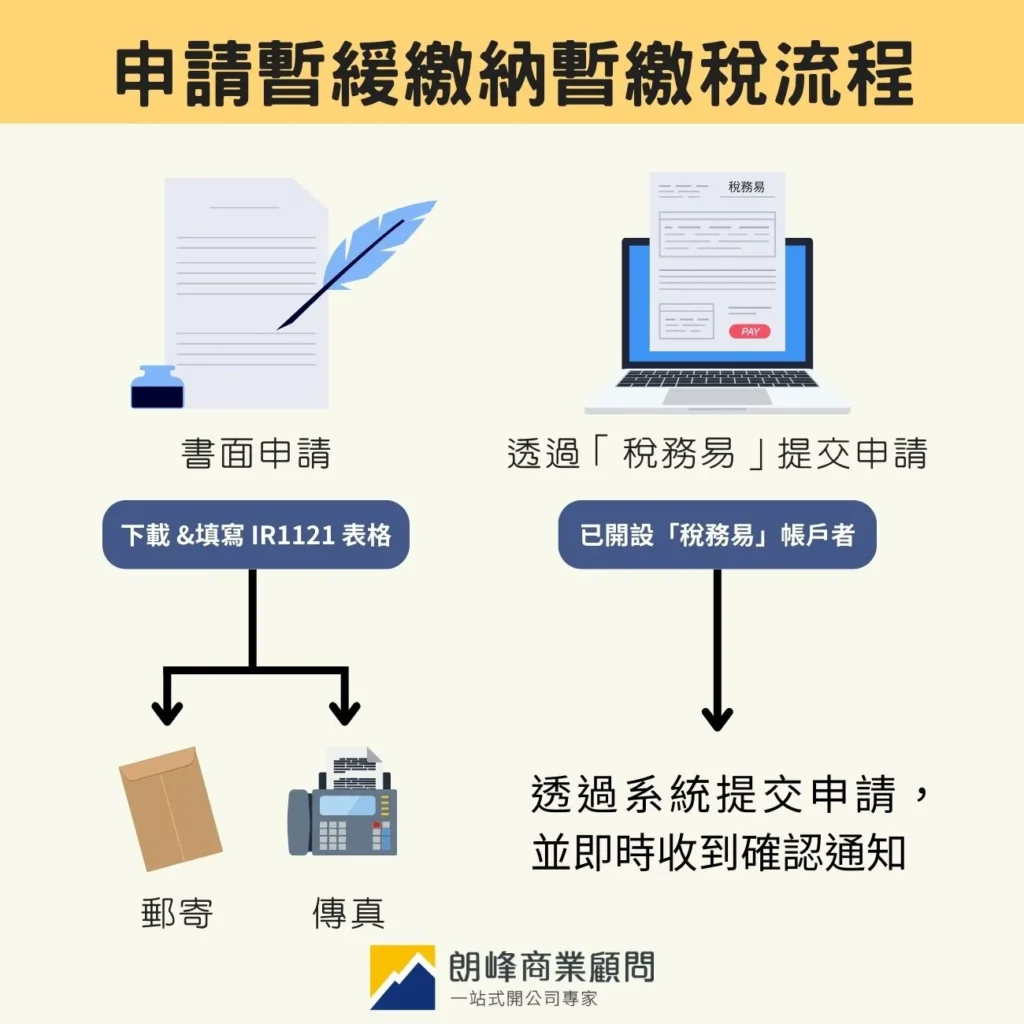

10. Method 1: Written application (IR1121 form).

- 11. On the tax authority's website.Download Form IR1121

- 12. Fill in the tax bill number, payment date, and reason for application.

- 13. Choose one of the following submission methods:

| way (of life) | 14. Details. |

|---|---|

| 15. Taxation Center, 5 Coordinating Road, Kai Tak, Kowloon, Hong Kong, Attention: Commissioner of Inland Revenue. | |

| 16. Fax. | 2519 6896 |

17. Method 2: eTAX online application.

18. For those who have opened an account, applications can be submitted directly through the system and receive immediate confirmation, which is more convenient than written applications.Tax easy19. The deferred amount is calculated based on the proportion of income reduction. For example, if the expected income decreases by 20%, the provisional tax can be correspondingly reduced by about 20%. Meeting the application criteria does not mean that provisional tax can be fully exempted; the tax authority will assess the final amount that can be deferred based on the information and reasons provided.

Frequently Asked Questions

How much temporary tax can be reduced after applying for deferred payment?

The deferred payment amount is calculated based on the proportion of income reduction. For example, if the expected income decreases by 20%, the provisional tax can be correspondingly reduced by about 20%. Meeting the application criteria does not mean that provisional tax can be fully exempted; the tax authority will assess the final amount that can be deferred based on the information and reasons provided.

Can the deferred tax be refunded?

Provisional tax is generally not refunded directly, but is offset after the formal assessment in the following year. If the actual taxable amount is lower than the provisional tax paid, the excess will be carried forward to offset the next assessment; if the taxpayer has stopped working or retired, the excess can also be applied for a refund.

What are the consequences of falsely reporting reasons to apply for deferred payment?

Falsifying applications constitutes tax evasion. According to the "Inland Revenue Ordinance," upon conviction, each charge can result in a maximum imprisonment of three years and a fine of HK$50,000, in addition to a penalty equivalent to three times the amount of tax underpaid.

Will the one-time relief for the 2025/26 fiscal year be reflected in the provisional tax?

No. The 2025/26 tax year 100% salary tax reduction (capped at HK$3,000) only applies to the final assessment, and provisional tax is not deductible; taxpayers must pay on time.

What is the relationship between the provisional salary tax and the final assessment tax bill?

Both are usually issued together on the same tax bill. The tax bill will specify the final assessment amount (the difference or refund after deducting provisional tax) and the provisional tax amount for the next year, indicated in different columns.

Conclusion

Provisional tax is a prepayment mechanism in the Hong Kong tax system, and understanding its calculation principles helps with cash flow planning in advance. If a significant decrease in income is anticipated for the next year, or if there are new allowances not yet reflected in the provisional tax notice, it is advisable to assess early whether the conditions for deferral are met and to submit an application before the deadline.

If you need assistance in assessing eligibility for deferral applications or filing taxes, you can learn more.Longfeng Tax Filing Services。

Extended Reading:

Complete guide to calculating salaries tax and personal tax exemptions.

Complete claim conditions for tax exemption for supporting parents

Tax exemptions for married individuals and strategies for joint filing.

Tax reporting tutorial for self-employed individuals/Freelancers

Last updated: May 2026.