Companies engaged in business and earning local profits in Hong Kong are required to pay profits tax. Limited companies adopt a two-tier tax rate (8.25% / 16.5%), while the tax rate for unlimited companies is 7.5% / 15%.

Summary of key points

- Hong Kong profits tax only applies to profits generated in Hong Kong, and overseas profits can apply for exemption.

- The two-tier tax rate for limited companies: the first HK$2 million at 8.25%, thereafter at 16.5%; for unlimited companies, it is 7.5% / 15%.

- The deadline for Class D for the year 2025/26 is August 15, 2026, and for Class M is November 16, 2026.

- The maximum penalty for late tax filing is HK$10,000 plus three times the tax amount, and in severe cases, imprisonment for 3 years may be imposed.

- Tax savings must be operated through professional accountants; incorrect tax filings, even if unintentional, may face penalties.

What is profits tax?

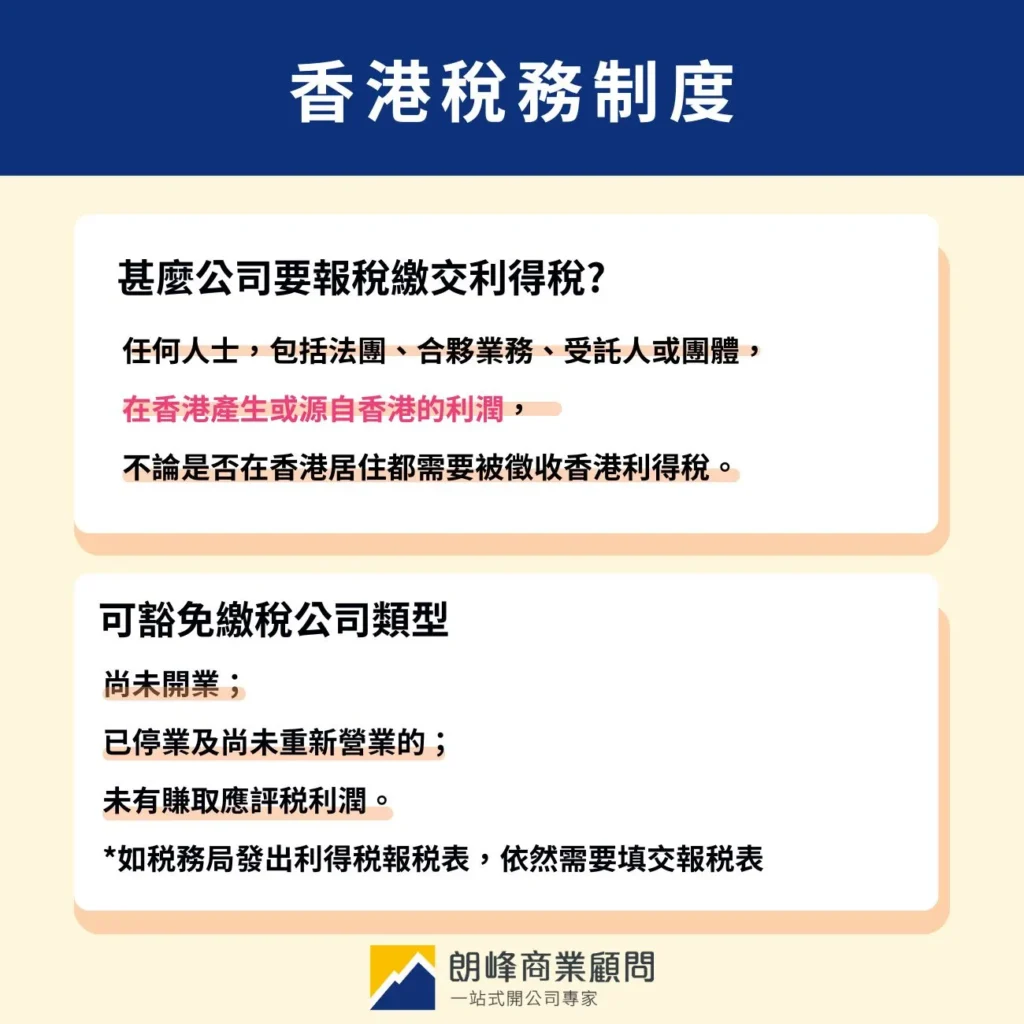

Profits Tax is a tax levied by the Hong Kong government on individuals engaged in any industry, profession, or business in Hong Kong and earning profits.

Hong Kong adopts the "territorial principle," which only applies toprofits generated in Hong Kong or derived from Hong Kong.Taxation. If business profits solely originate from outside Hong Kong, taxpayers can apply for offshore income exemption from taxation and are not required to pay profits tax in Hong Kong.

Situations where profits tax must be paid:

- Operating any industry, profession, or business in Hong Kong

- Earning profits from that business

- The relevant profits are generated in Hong Kong or derived from Hong Kong.

The applicable subjects include limited companies, unlimited companies (sole proprietorships and partnerships), trustees, and organizations, regardless of whether they reside in Hong Kong.

Extended Reading:Unlimited company tax filing cheat sheet: profits tax calculation, deduction checklist, and reporting highlights.

Which businesses can be exempt from tax filing?

In the following situations, the tax authority will not proactively request the submission of tax returns, but once issued, they must still be filled out according to regulations:

- Businesses that have not yet commenced operations

- Businesses that have ceased operations and have not yet resumed

- Businesses that have not earned assessable profits

💡 Longfeng reminds youExemption from tax filing does not equate to permanent non-filing. The tax authority may still issue tax returns to the above businesses when reviewing potential tax liabilities, and they must be submitted on time, or face penalties.

Hong Kong profits tax rates (two-tier system)

Hong Kong adoptsa two-tier profits tax rateto alleviate the tax burden on small and medium-sized enterprises.

limited company

| Profit tiers. | tax rate |

|---|---|

| First HK$200 million | 8.25% |

| The portion exceeding HK$2 million | 16.5% |

Unlimited company (sole proprietorship/partnership)

| Profit tiers. | tax rate |

|---|---|

| First HK$200 million | 7.5% |

| The portion exceeding HK$2 million | 15% |

NoteWhen a group has multiple subsidiaries, a groupcan only have one subsidiary at most.Declare the two-tier tax rate, and other subsidiaries must be taxed at the standard tax rate (15% or 16.5%).

Calculation example (limited company)

Example 1: Profit HK$1,000,000 Less than HK$2 million, calculated entirely at 8.25%:

HK$1,000,000 × 8.25% = HK$82,500

Example 2: Profit HK$3,000,000 The first HK$200 million at 8.25%, the remainder at 16.5%:

(HK$2,000,000 × 8.25%) + (HK$1,000,000 × 16.5%) = HK$165,000 + HK$165,000 = HK$330,000

Company Tax Returns

The declaration methods for unlimited companies and limited companies are different:

| limited company | Unlimited company (sole proprietorship) | Unlimited company (partnership) | |

|---|---|---|---|

| Declaration form | BIR51 | BIR60 (individual tax return) | BIR52 |

| Declaration method | Independent declaration | Declare in the owner's personal tax return | Independent declaration, partners must also declare their share of profits in BIR60 |

2025/26 tax return extension arrangements

Profits tax return is sent out every year On the first working day of AprilIn succession, and must be returned to 2. fill out the IRBR200 to notify the tax bureau within 1 month, declaring the actual nature of the business.the tax bureau.

Deadline for batch extension for the 2025/26 tax year

| Code | Accounting settlement date range | Deadline | Electronic tax return deadline |

|---|---|---|---|

| Category N | April 1 – November 30 | No extension (around early May) | 1 month longer than the normal deadline |

| Category D | December 1 – December 31 | August 15, 2026 | September 15, 2026 |

| Category M | January 1 – March 31 | November 16, 2026 | December 16, 2026 |

| M category (loss for this year) | January 1 – March 31 | February 2, 2027 | March 2, 2027 |

Source: Tax Bureau Tax Representative Circular —Regarding the arrangement for batch extension submission of the 2025/26 tax return

💡 Longfeng reminds you: Extensions do not take effect automatically and must be submitted through a tax representative for a batch extension application (Block Extension). Using eTAX allows for an additional automatic 1-month extension, which is the most convenient way.

Deductible items: Company daily expenses

Necessary expenses incurred to generate assessable profits can be claimed for deduction:

✅ Deductible items

- Rent for office, warehouse, or shop, rates, management fees

- Employee salaries, allowances, bonuses

- Employer MPF (mandatory and voluntary) contributions

- Cost of goods sold and raw materials

- Utilities, telephone, internet fees (must be proven for business use)

- Insurance premiums related to business (labor insurance, corporate group medical insurance, etc.)

- Accountant fees and other professional service fees

- Bad debts, doubtful debts

- Entertainment expenses

❌ Non-deductible items

- Household or personal expenses

- Capital expenditures (e.g., renovations)

- Salaries and capital interest of sole proprietors or partners themselves

- Various taxes paid under the "Tax Ordinance" (excluding salaries tax)

- Contributions to unrecognized occupational retirement schemes

Special tax deduction items

| Project | Deduction method |

|---|---|

| Expenditure on building renovation | Equal deductions over 5 years starting from the actual payment year |

| Computer hardware and software | Full deduction of expenses incurred during the assessment period |

| Environmental facilities (electric vehicles, food waste machines, etc.) | Full deduction of expenses incurred during the assessment period |

| Restoration of leased premises expenses | Expenses for restoring leased properties to their pre-leasing condition are deductible (effective from 2024/25) |

| Tax exemption for industrial/commercial buildings | The claim deadline has been removed; new owners can still claim tax exemptions for the property upon transfer |

| Charitable donations | Not less than HK$100, with a cap of 35% of assessable profits |

Consequences of late submission of tax returns

Timely filing of tax returns is a legal obligation of taxpayers. The consequences of late submission are as follows:

According toInland Revenue OrdinanceA penalty may be imposed for late submission of profits tax returns HK$10,000 and must be paidthree times the tax amountand may face prosecution. In serious cases (such as failure to provide sufficient income and expenditure records, incorrect tax filing), the maximum penalty may be HK$50,000 three times the tax amount and imprisonment for 3 years。

Legal tax-saving strategies

Profits tax is calculated based on "assessable profits," and the core of legal tax-saving lies inaccurately reporting all deductible expensesrather than self-judging which items are deductible.

Common tax-saving directions:

- Fully report business expenses: Ensure all eligible expenses have receipts and are accurately reported

- Make good use of depreciation allowancesAssets such as machinery, equipment, and computers can be deducted based on depreciation rates.

- Apply for offshore income exemption.If business income meets offshore conditions, tax exemption can be applied for.

- Make good use of charitable donation deductions.Donations to recognized charitable organizations can be deducted, with a limit of 35% of assessable profits.

💡 Longfeng reminds youTax planning must involve a professional accountant; do not make your own judgments on whether an item is deductible. Incorrect tax reporting, even if unintentional, still faces the risk of penalties.

Extended Reading:Audit service content for Hong Kong companies.

Frequently Asked Questions

Does a loss-making company still need to submit a profit tax return?

Required. Even if the company incurs losses, tax returns must still be submitted on time. The loss amount can be carried forward to future years to offset future assessable profits.

Do overseas income need to be taxed in Hong Kong?

Hong Kong adopts a territorial source principle, and if profits are purely derived from outside Hong Kong, an offshore income tax exemption can be applied for. However, the determination of "offshore source" has strict criteria and must be assessed by a professional consultant; self-declaration is not allowed.

Do self-employed individuals also need to pay profits tax?

Required. Self-employed individuals operating a business in Hong Kong and earning profits must also pay profits tax on assessable profits, reported in the personal tax return (BIR60).

Extended Reading:How do freelancers file taxes? A guide for self-employed individuals.

What is provisional income tax?

The tax authority collects a portion of the profits tax for the next year in advance based on the assessable profits of the previous tax year. If the actual tax payable exceeds the amount already paid, the difference must be paid; if overpaid, it can be refunded or offset against the next year's tax.

Extended Reading:Temporary tax calculation method at a glance.

Do shareholders need to pay additional income tax on the dividends they receive?

No need. Hong Kong dividends are post-tax distributions, and the company has already paid profits tax on its profits; shareholders generally do not need to pay tax again when receiving dividends.

Extended Reading:Do Hong Kong dividends incur tax? A comprehensive analysis of taxation.

Let the professionals handle tax filing; Longfeng Business Consultants will help you sort it out.

Tax reporting involves a lot of details, and incorrect or omitted reporting carries legal risks. Longfeng Business Consultants provide professional profits tax reporting and tax planning services to assist you in compliant reporting and legal tax savings, allowing you to focus on business development.

to book a free consultation |Understand Longfeng's tax filing services.

Extended Reading

Company tax filing tutorial for employees: What is the difference between BIR56A and IR56B?

Do Hong Kong dividends incur tax? A comprehensive analysis of taxation.

Temporary tax calculation method at a glance.

How do freelancers file taxes? A guide for self-employed individuals.

Audit service content for Hong Kong companies.

Tax authority Kai Tak address, subway exit, and office hours.

Last updated: May 2026 | Data is based on the official announcement from the tax bureau