Unable to open a company account? Understand the conditions for opening a bank account in Hong Kong and the 4 major reasons for rejection in this article.

The rejection of Hong Kong company account openings mostly stems from four points: high business nature risk, incomplete documents, questionable director backgrounds, or address proof not meeting requirements.

Summary of key points

- Reasons for rejection: unclear business nature, document issues, director background, invalid address proof

- Address proof must be issued by a government or financial institution and must be within the last 3 months.

- Non-Hong Kong resident directors face higher application difficulties and need to prepare additional proof of business contact in Hong Kong.

- The account opening process for virtual banks is simple, but service functions are limited and must be chosen according to business needs.

- How difficult is it to open a Hong Kong company account? The current situation is clear at a glance.

How difficult is it to open a Hong Kong company account? The current situation is clear at a glance.

Many entrepreneurs mistakenly believe that once a company is successfully registered, opening a bank account is just a formality. However, in recent years, Hong Kong banks haveFinancial Management Bureausignificantly tightened their review standards under increasing anti-money laundering (AML) regulatory pressure, with the average processing time for SME account applications extended to 4-8 weeks, and complex cases even exceeding 3 months, causing many newly established companies to hit a wall on their first application.

The industry generally reflects that some traditional banks have a high rejection rate for newly established companies, especially those involved in cryptocurrency, cross-border e-commerce, or companies with non-local Hong Kong clients, where the scrutiny is even stricter.

The core concern of banks is singular: does this company have a real business? Is the flow of funds legal and explainable? All review standards revolve around these two points.

Necessary conditions and documents for applying for a company account

Basic application requirements

Before opening an account, first confirm whether the company meets the basic thresholds of the bank. The following 4 points are commonly required standards by major banks, and none can be missing:

- The company has completed formal registration with the Hong Kong Companies Registry and holds a valid Certificate of Incorporation (CI) and Business Registration Certificate (BR)

- At least one director is a natural person (not all corporate shareholders)

- Directors and shareholders can personally attend the bank account opening interview (some banks can arrange video calls)

- The company is not involved in restricted industries (such as unlicensed lending, remittance, and other regulated businesses)

Required documents for account opening (Overview of 3 main categories)

Account opening documents can be roughly divided into 3 categories, as shown in the table below for your reference:

| Category of Documents | Main content | Remarks |

|---|---|---|

| Company statutory documents | Certificate of Incorporation (CI), Business Registration Certificate (BR), Articles of Association (M&A), list of shareholders and directors | Certified true copies (CTC) must be provided |

| Director/Shareholder identity documents | Original Hong Kong Identity Card or passport, address proof (utility bill or bank letter within the last 3 months) | Foreign directors need to provide additional proof of residential address |

| Business description document | Business plan or business description letter, client/supplier list (can be anonymous), contract samples or quotation forms | Such documents are often the key to the success or failure of account opening |

For a more detailed list of required documents, please refer to the article below.

Extended reading: "TheWhat documents do I need to bring to open a company account, 3 major types of documents to help you open a company account quickly》

Choose the appropriate type of bank

The account opening thresholds of various banks in Hong Kong vary significantly; choosing the wrong type can be more detrimental than having incomplete documents, especially a record of being rejected by a large bank may affect the review impression of other banks.

| Bank Type | Representative examples | Account opening thresholds | Suitable audience |

|---|---|---|---|

| Large traditional banks | HSBC, Bank of China, Hang Seng | The strictest, interviews are mandatory, review period 1-4 weeks | Companies with mature businesses, fixed clients, and transaction records |

| Small and medium-sized local banks | Public Bank, Chiyu Bank | Relatively lenient, some can be reviewed by mail | Startups, simpler local businesses |

| Virtual banks | Airwallex, Neat, Statrys | Fully online application, faster review (from a few days to 2 weeks) | Cross-border payments, e-commerce, startups, higher acceptance rate |

The four main reasons for company account application rejection

Reason 1: Unclear business nature or belongs to a high-risk industry

Banks need to clearly understand what the company "does, where the money comes from, and where the money goes." If the business description is vague, or if the business itself falls into a high-risk category defined by the bank, the application is often blocked at the first hurdle.

Common business types considered high-risk:

- Cryptocurrency-related businesses (buying and selling, wallets, NFT platforms)

- Cross-border remittances or currency exchange

- Major clients from sanctioned countries or regions

- Business involves a large amount of cash transactions

- Description is too vague (e.g., only stating "engaged in trade" without specifying goods and counterparties)

Prepare a 1-2 page business description before applying, detailing what the company does, where the main clients are, payment methods, and the flow of funds. This document often has a greater impact on the review outcome than all other documents combined.

Reason 2: Incomplete document preparation

Companies with fully compliant business nature are also often rejected due to document issues. The most common situations are:

- Address proof dated over 3 months, or using unacceptable document types (e.g., handwritten receipts)

- Company documents lack certified copies (CTC)

- Director signatures do not match the spelling of names on identification documents

- Company articles (M&A) version not updated to the current shareholder structure

Reason 3: Issues with director backgrounds

Banks will conduct background checks (KYC) on each director and major shareholder. The following situations significantly reduce the success rate of account opening:

- Directors or shareholders from countries classified as high-risk by FATF

- Directors have problematic personal credit records or have been blacklisted by banks

- Company shareholder structure is complex (e.g., multi-layer holding companies), making it difficult to trace the ultimate beneficial owner (UBO)

- Directors cannot attend the interview in person, or their attitude during the interview is vague and unable to clearly explain the business.

If the company's shareholder structure involves foreign holding companies, it is recommended to prepare a complete set of documents and organizational charts for the relevant companies in advance, so that the bank can clearly trace back to the ultimate natural person owner.

Reason four: Strict requirements for address proof.

Banks have very strict requirements for address proof, which must be a formal document issued within the last 3 months by a government agency, utility company, or financial institution, clearly showing the applicant's name and address.

The following documents are usuallyNot accepted:

- Mobile phone bill

- Insurance company letter

- Online shopping platform bill

If the director is a tenant or lives with family and cannot provide a bill registered in their own name, they can use a bank statement or a residence declaration issued by the landlord/family, along with their identification and proof of address. Confirm the acceptable document types with the target bank before applying to avoid unnecessary trips.

Extended reading: "TheCan I use a virtual office for my business registration address? Requirements, change of address process in one article to see clearly》》

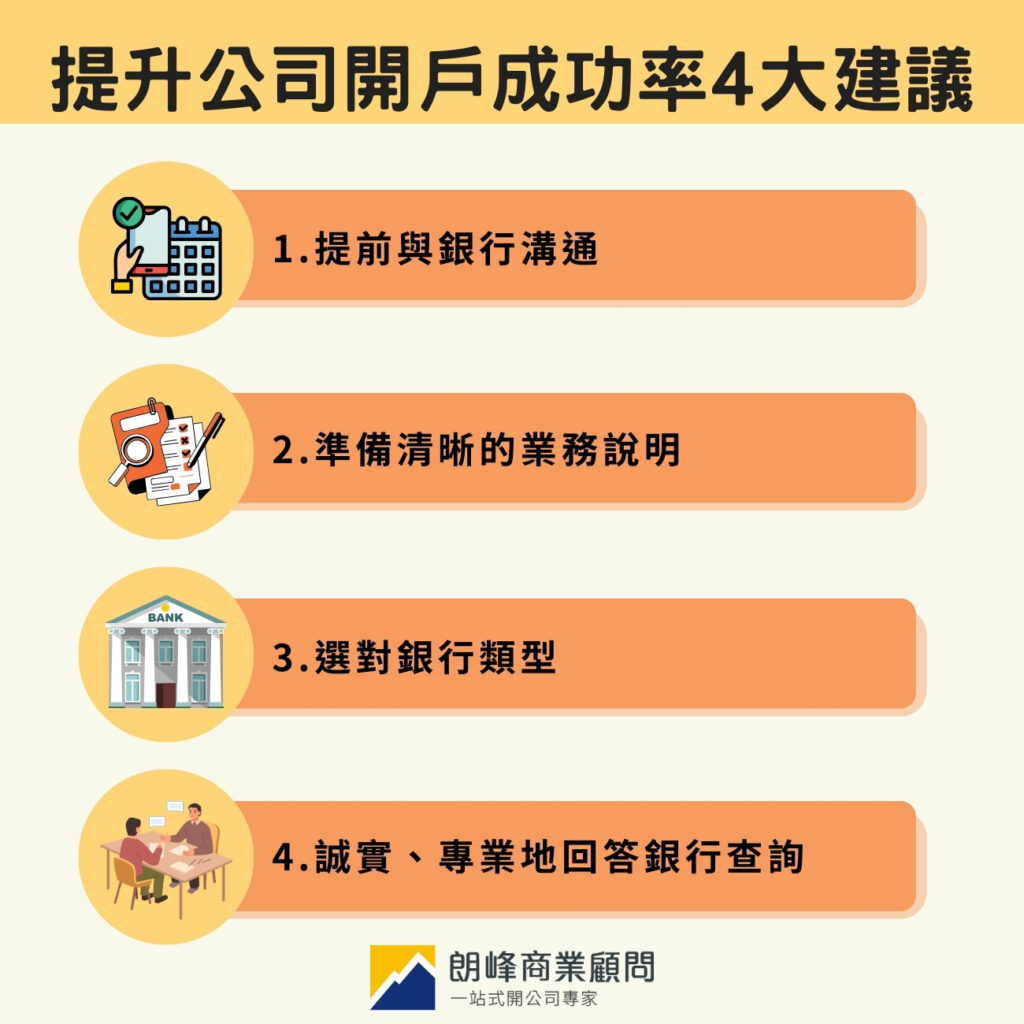

Longfeng's warm reminder: 4 major suggestions to improve the success rate of company account opening

- Communicate with the bank in advance

Contact the account manager before applying to understand the bank's account opening policies for specific industries. Some banks have internal restrictions on certain industries, and confirming in advance can save time.

- Prepare a clear business description

Be able to clearly answer questions about the business model, sources of income, target customer group, and expected transaction volume, and attach the website, promotional materials, or letters of intent. The core question for the bank's review is: "Does this company have a real business?"

- Answer bank inquiries honestly and professionally

Answer truthfully during bank inquiries, and do not be vague or deliberately avoid questions. Good communication helps build trust, and trust is often key to approval.

- If rejected, understand the reasons before reapplying.

After being rejected by one bank, do not immediately apply to multiple banks at the same time. First, inquire about the reason for the rejection, improve based on the issues, and then reapply; the success rate will significantly increase.

Frequently Asked Questions

How long does it take to open an account?

Generally takes 4-8 weeks, complex cases may exceed 3 months. The approval time for virtual banks is usually shorter, and some cases can be completed within a few working days.

Can I open multiple accounts at the same time?

Yes. Enterprises can open accounts at different banks based on business needs, such as using traditional banks for main operations and virtual banks for daily collections, allowing for flexible combinations.

Can I apply again after being rejected?

Yes, but it is recommended to first understand the reason for the rejection, and then apply to other banks after improving the issues. Repeatedly applying to the same bank in a short period usually does not have a high success rate.

What is the difference between virtual banks and traditional banks?

The process of opening an account with a virtual bank is simpler, but it usually does not support check services, cash deposits, or international wire transfers, and the daily transaction limit is also lower. Traditional bank services are more comprehensive and suitable for businesses with complex transaction needs.

Account opening rejected? Longfeng Business Consultants help you get it right the first time

Account opening rejection is often not a document issue, but rather a problem with the preparation direction. Longfeng Business Consultants provide bank account opening assistance services, covering pre-application assessment, document organization, bank selection advice, and interview coaching to help you target the right solutions and improve success rates. For more details, please feel free toBooking Enquiry。

Extended reading: "TheComplete guide to starting a company in Hong Kong: processes, costs, and precautions》