What to do after setting up a Hong Kong company? A comprehensive summary of statutory matters and deadlines that must be completed in the first year.

The first year after the establishment of a Hong Kong company must complete opening a bank account, setting up an accounting system, submitting the annual return (NAR1), declaring profits tax, and renewing the business registration, each with a clear statutory deadline, missing which will incur fines.

Summary of key points

- The annual return must be submitted within 42 days after the anniversary of the establishment.

- The profits tax return form is usually received about 18 months after establishment and must be submitted within 1 month of receipt.

- The business registration certificate must be proactively renewed before it expires; one cannot just wait for the tax authority to notify.

- All business documents must be kept for at least 7 years for tax authority audits.

- The year-end date involves tax filing deadline classification and audit scheduling, so it should be determined as early as possible.

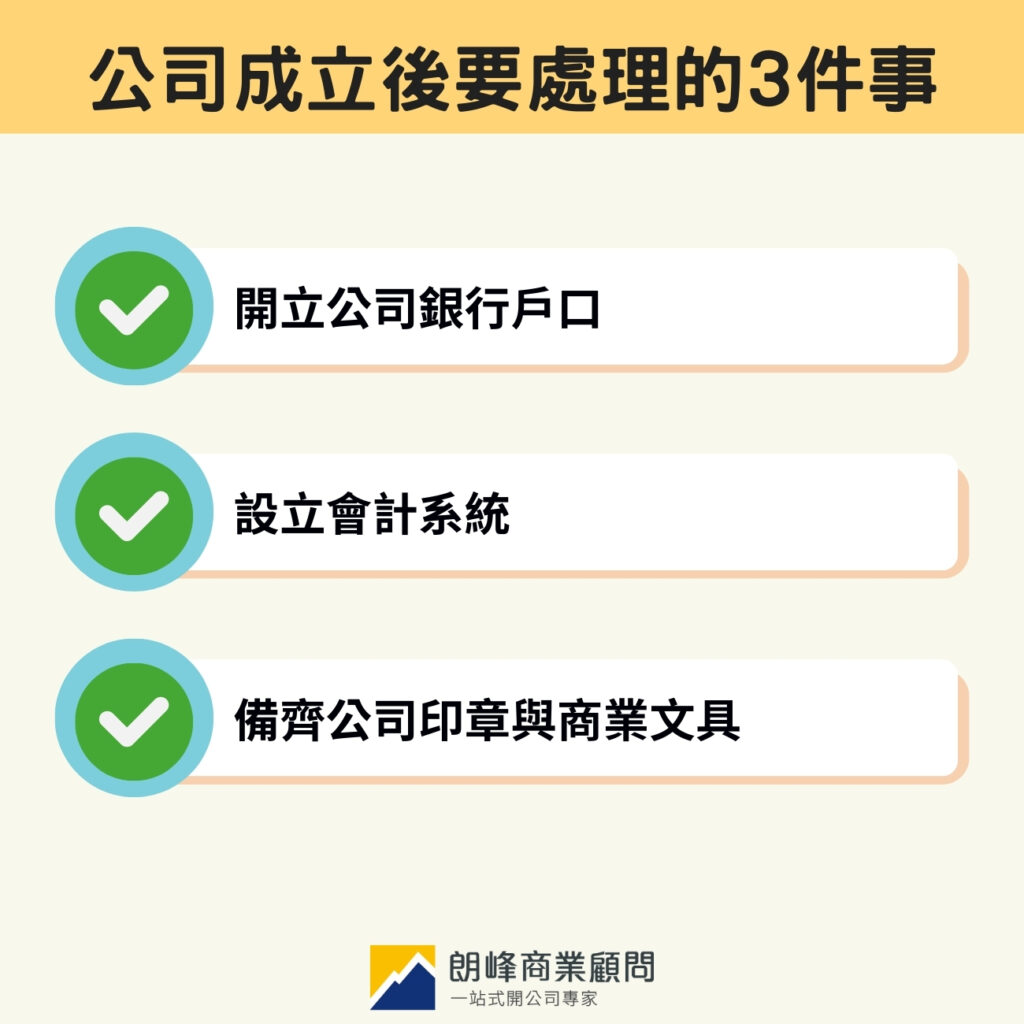

Three things to handle immediately after the company is established.

Opening a company bank account: traditional banks vs virtual banks.

Opening a company bank account is the top priority after establishment. Required documents include the company registration certificate, business registration certificate, articles of association, identification and address proof of directors and shareholders. Traditional bank approvals usually take 4–8 weeks, while virtual banks can complete account opening in a few days.

For companies with cross-border business, it is recommended to prioritize banks that support multiple currencies and international remittances. Some banks have stricter account opening reviews for new companies, so preparing complete business description documents in advance can significantly increase the success rate.

Extended reading: "TheUnable to open a company account? Understand the conditions for opening a bank account in Hong Kong and the 4 major reasons for rejection in this article.》

Setting up an accounting system.

According to Section 373 of the Companies Ordinance, all limited companies must maintain proper accounting records covering income and expenses, assets and liabilities, and sales and purchase details. The tools do not need to be perfect from the start; initially, Excel can be used for recording, and later upgraded to professional software like Xero or QuickBooks as the business grows. Regardless of the method chosen, all original documents and invoices must be kept for at least 7 years for tax authority audits.

The choice logic between outsourcing bookkeeping vs doing it in-house.

The most common issue faced by startups is: when is it worth outsourcing? Here are some simple judgment criteria:

- If the monthly transaction volume is less than 50 and there are no employees—it's advisable to handle it in-house using Excel or basic software.

- If the monthly transaction volume exceeds 50 or there are employee salaries—it's recommended to hire an accountant or a secretarial company, with a monthly fee of about HK$800–$2,500.

- If there are cross-border transactions, multiple currencies, or a complex equity structure—it's advisable to outsource as early as possible to avoid having to reorganize everything at year-end.

The earlier the accounting records are established, the better; waiting until just before year-end to catch up is often the main reason for doubled costs.

Prepare the company seal and business stationery.

The Companies Ordinance has removed the mandatory requirement for a corporate seal, but in practice, some companies still keep one for statutory documents like share certificates, costing about a few hundred Hong Kong dollars. Company letterheads must, according to Section 101 of the Companies Ordinance, state the company name, registration number, and address, which are basic requirements and cannot be omitted.

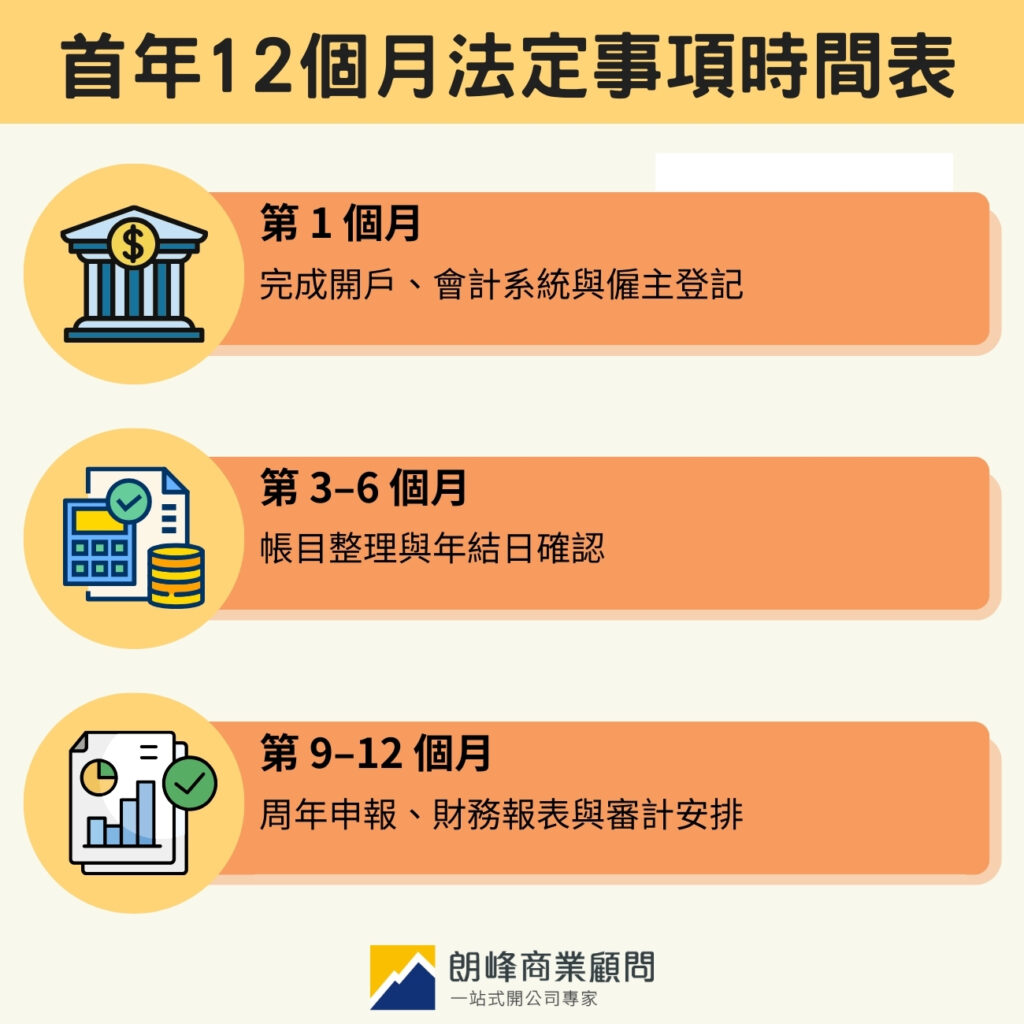

Statutory timeline for the first 12 months (including fine reminders).

| Time | Mandatory tasks. | Points of Attention |

|---|---|---|

| Month 1. | Open a bank account, set up an accounting system, confirm the company secretary and registered address. | When hiring employees, apply for an employer tax number simultaneously. |

| Months 3-6. | Regularly update accounts, retain business documents, and confirm the financial year-end date. | The year-end date affects subsequent audit scheduling and tax filing categories. |

| Months 9–12. | Submit the first NAR1, hold the annual members' meeting, and prepare financial statements. | Late submission of NAR1 incurs a fine, with no grace period. |

| Around the 18th month. | Receive the profits tax return (BIR51), which must be submitted within one month. | You can apply to the tax authority for a 2–3 month extension. |

Month 1: Open an account, set up accounting systems, and register as an employer.

In addition to the bank and accounting systems, if the company plans to hire employees, it must apply for an employer tax file number from the tax authority this month and understand the contribution requirements for the Mandatory Provident Fund (MPF). The arrangements for the company secretary and registered address should also be confirmed at this stage to ensure normal receipt of government correspondence and legal documents.

Months 3–6: Organize accounts and confirm the year-end date.

The most important task at this stage is to determine the financial year-end date, as it directly affects the classification of tax filing deadlines (N/D/M categories) and the starting point for audit work. At the same time, systematically organize accounts and retain receipts to prepare for future audits, rather than searching for documents all at once at year-end.

How to choose a year-end date?

Although there are no hard rules for the year-end date, choosing different dates has practical implications for the company:

- Choose March 31.: It falls under Category M, with a tax filing deadline extended to November 15 of the same year, allowing for the longest preparation time, which is the most common choice for startups.

- Choose December 31.: It falls under Category D, with a tax filing deadline of August 15 of the following year, aligning with the calendar year, making account management more intuitive.

- Choose around the anniversary of establishment.: NAR1 coincides with the year-end period, allowing for centralized compliance handling, but the workload will also be concentrated.

Once the year-end date is confirmed, any future changes need to be notified to the tax authority and may affect tax filing arrangements; it is advisable to consult an auditor early in the establishment phase.

Months 9–12: Annual filing, financial statements, and audit arrangements.

The first NAR1 must be submitted within 42 days after the company's anniversary date. If the financial statements do not meet the small company exemption criteria, they must be audited and presented at the annual general meeting. This stage has the most concentrated workload, so it is recommended to start organizing relevant documents three months in advance; otherwise, it can easily become chaotic as the deadline approaches.

What is the annual return form (NAR1)?

According to Section 662 of the Companies Ordinance, private limited companies must submitCompanies RegistryNAR1 annually to update registration information such as directors, company secretary, shareholders, and registered address to ensure accurate records.

The registration fee for timely submission is HK$.105Once overdue, the fine will increase over time:

| Overdue time. | Fine amount |

|---|---|

| Exceeding 42 days, not exceeding 3 months | HK$870 |

| Exceeding 3 months, not exceeding 6 months | HK$1,740 |

| Exceeding 6 months | HK$3,480 |

In severe cases, the company and directors may be prosecuted, with a maximum fine of HK$50,000. Continued delays may even lead to the company being struck off and dissolved, with risks far exceeding the fines themselves. For steps, precautions, and common mistakes in filling out the NAR1, please refer to the following article.

Extended Reading:

《4 Points to Note for Submitting Annual Returns》

Profits tax filing guidelines.

The profit tax return for Hong Kong companies is actively issued by the Inland Revenue Department, not applied for by the company. New companies generally receive their first tax return (BIR51) about 18 months after establishment, and they have 1 month to submit it after receiving it. If there is not enough time, an extension can be requested, usually allowing for an additional 2-3 months, but it must be proactively submitted before the original deadline.

No business income in the first year still requires reporting.

Even if the company has no business income in the first year, it must still submit the tax return on time after receiving it. Those with no business activities can report.Zero reporting.If there are business activities but no income yet (for example, in the preparation stage), relevant expenses must still be reported with a brief explanation; it cannot be ignored just becausethere is no profit.it should still be submitted.

Losses are also important tax assets.

No tax is required for loss years, but the tax return must still be submitted. The loss amount can be carried forward to the next year to offset future profits, so do not overlook this step just because there is no profit.

For information on profit tax rates, two-tier calculation methods, deductible items, and the complete tax filing process, please refer to the article below.

Extended reading: "TheHong Kong Profits Tax Guide: Key Tax Points Every First-Time Entrepreneur Should Know》

Proactively renewing the business registration certificate before it expires is safer than waiting for a notification.

The validity period of the business registration certificate is either 1 year or 3 years. Although the tax authority will send out renewal notifications, it is recommended that companies mark the expiration date on their calendar upon establishment and handle the renewal one month in advance, rather than waiting for a notification to take action.

| Type | Fee |

|---|---|

| One-year certificate | HK$250 (additional fees apply, actual amount depends on the government's budget announcement for the year) |

| Three-year certificate | HK$3,950 (including fees) |

Can be processed on the tax authority's website, using credit card or PPS payment. Once completed, the business registration certificate will be mailed to the company's registered address. If lost, the reissue fee is HK$220, which can be applied for at the tax authority's business registration office.

Frequently Asked Questions

What happens if I miss the anniversary declaration meeting?

Fines start from HK$870 and increase according to the overdue period, up to a maximum of HK$3,480. In serious cases, directors may be prosecuted, with a maximum fine of HK$50,000. Continued violations may even lead to the company being struck off and dissolved, with consequences far more severe than the fines.

Is it necessary to report profit tax in the first year?

Even if the company has no business income, it must still submit the tax return on time after receiving it. Those with no business activities can file a "nil return"; if there are business activities but no income (e.g., in the preparation stage), relevant expenses must still be reported with a brief explanation attached.

Can I handle these compliance matters myself?

Technically feasible, but annual returns, tax filings, and financial statements all involve clear statutory requirements, and any detail errors may incur fines or legal liabilities. Unless one is quite familiar with Hong Kong company regulations, it is safer and more time-efficient to entrust a professional company secretary or accountant to handle it.

When does the business registration need to be renewed?

Although the tax bureau will send out notifications, there may be occasional delays in the mail. It is recommended that the company note the expiration date of the business registration certificate upon establishment and handle it one month in advance to avoid unnecessary fines due to momentary negligence.

Confused about company compliance matters? Let Longfeng Business plan it all out for you.

The compliance matters for the first year of a Hong Kong company are interconnected, and a delay in one link often affects all subsequent work. If you find it difficult to track the above matters on your own, entrusting a professional company secretary or accountant for unified management is a choice many entrepreneurs make. If needed, you can refer toLongfeng Businessthe services.

Extended reading: "TheComplete guide to starting a company in Hong Kong: processes, costs, and precautions》